13.1 |

Resources

•

A new

Stabilisation Aid Fund (SAF) would be established to “take on”

funding for

stabilisation

and reconstruction activity in “‘hot’ conflict zones” from the

Conflict

Prevention

Pool.

•

New

governance and programme management arrangements for the

Conflict

Prevention

Pool and the SAF would be introduced to ensure that activity

was

based on a

common strategy, and that expenditure was prioritised

effectively

against

that strategy.

649.

In December,

the PCRU was renamed the Stabilisation Unit (SU), reflecting

the

emergence

of the broader concept of stabilisation and the Unit’s new role

managing

650.

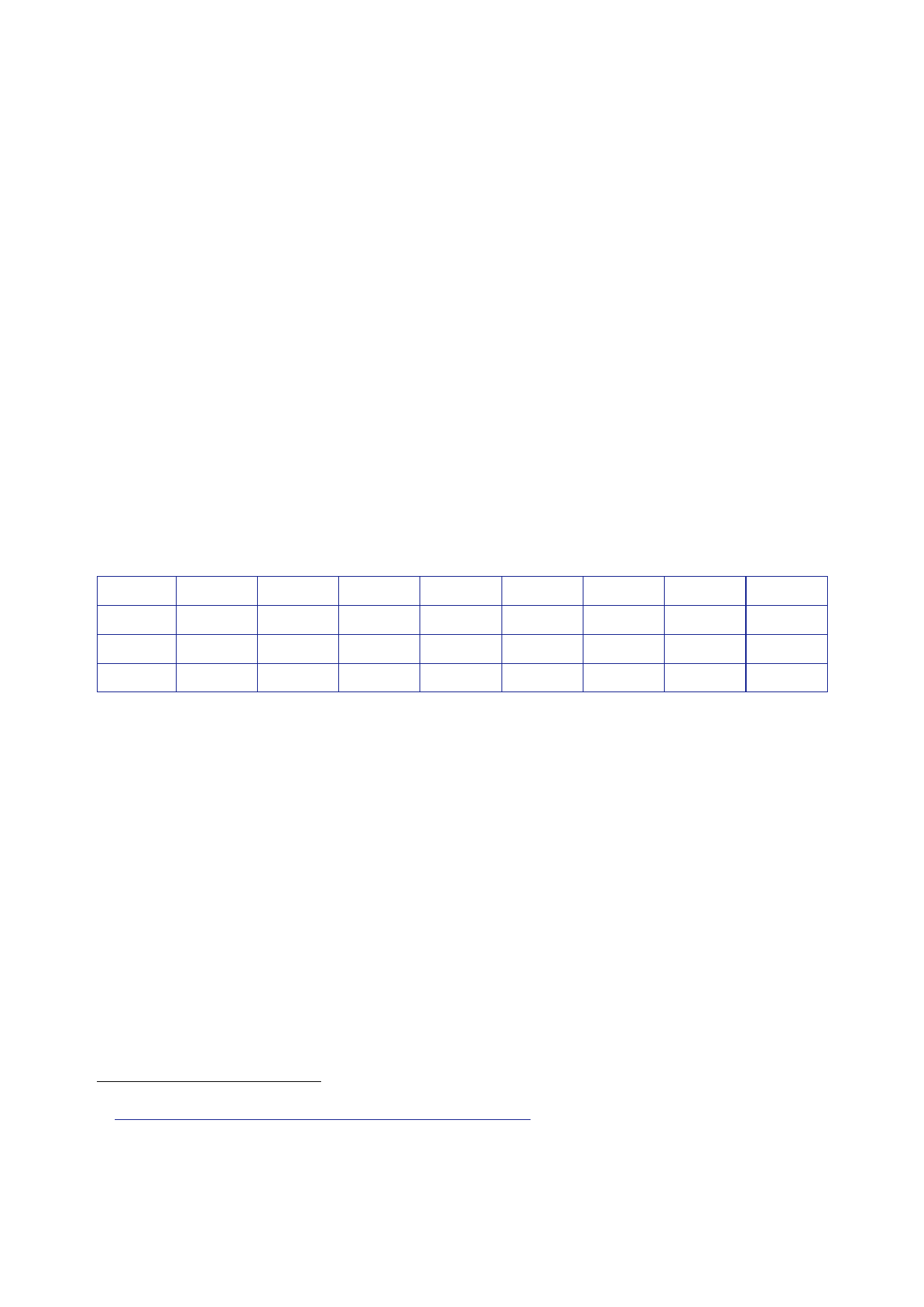

The table

below shows the departmental settlements for the MOD, the

FCO

and DFID

from 2002/03 to 2009/10 (under the 2002, 2004 and 2007

Comprehensive

MOD

FCO

DFID

2002/03

28.0

1.5

3.9

2003/04

29.0

1.5

4.0

2004/05

29.2

1.6

4.0

2005/06

29.9

1.7

4.9

2006/07

30.2

1.7

5.3

2007/08

30.2

1.6

5.5

2008/09

30.8

1.6

5.7

2009/10

31.1

1.6

6.6

651.

The Inquiry

describes earlier in this Section how the MOD reclaimed the

net

additional

costs of military operations (NACMO) from the Reserve under an

established

procedure.

652.

All other

departments sought to cover additional costs by reprioritising

within their

existing

budgets and, if and when that proved insufficient, bidding to the

Treasury to

secure

additional funding from the Reserve.

653.

In his

evidence to the Inquiry, Sir Mark Lyall‑Grant described the

different levels

of funding

available to departments:

“… you have

the MOD which can call on the Reserve for unforeseen

military

expenditure.

You have DFID, who have a large amount of programme money,

but

403

Paper

Stabilisation Unit, December 2007, ‘Stabilisation

Unit’.

404

Email

Treasury [junior official] to Iraq Inquiry [junior official], 17

April 2014, ‘Further Queries Relating

to

Resources’. Figures are near cash settlements, in real terms

(2008/09 prices). Figures may differ from

Comprehensive

Spending Review settlement letters due to budget exchange,

inter‑departmental transfers

and other

factors.

551